Complete Guide to AI Voice Agents for Mortgage Lending

Marr Labs

January 14, 2026

AI voice agents are rapidly becoming core mortgage infrastructure. This guide shows how they actually work, where they drive real ROI, and what it takes to deploy them safely at scale without breaking compliance or borrower trust.

Introduction

Mortgage lending is hitting a structural reset. Borrowers expect instant, 24/7 answers, Loan Officers are juggling more communications channels than ever, and the cost to originate a loan keeps creeping up. AI voice agents are emerging as one of the few levers that can move all three constraints–speed, cost, and borrower experience—at once.

For top mortgage lenders, voice AI is no longer a novelty. It’s becoming infrastructure: qualifying leads in minutes, orchestrating complex workflows, and enforcing compliance at scale. Early adopters are already reporting double-digit improvements in worked opportunities and cycle time compression measured in days.

This guide is written for modern mortgage executives, technologists, and revenue leaders who want a complete picture: what AI voice agents are, how they work with your LOS and CRM, how to stay compliant, what implementation really looks like, where the risks are, and how to measure ROI.

Table of Contents

What Are AI Voice Agents?

Why Mortgage Lenders Need Voice AI Now

How AI Voice Agents Work (Technical Architecture)

Core Mortgage Use Cases

Compliance and Risk Management

Implementation and Integration (8–12 Week Plan)

Measuring ROI and KPIs That Matter

Real-World Impact and Marr Labs Example

Challenges, Risks, and How to De-Risk Adoption

The Future of Voice AI in Mortgage

FAQ

What Are AI Voice Agents?

From IVR to Agentic AI

Legacy IVRs and basic phone trees were built to route calls and reduce headcount, not to understand borrowers. They forced people into rigid menus and handed off context-poor calls to overloaded loan officers.

They understand natural speech using advanced speech-to-text and NLP.

They maintain context over multi-step conversations and across channels.

They take actions like scheduling and updating LOS/CRM without human intervention.

In other words, they behave less like automated receptionists and more like digital loan officer assistants that operate 24/7.

Core Technologies in Plain English

Under the hood, a production-ready voice agent combines:

Speech recognition: Converting borrower speech to text in real time with high accuracy, including different accents and noisy environments.

Natural language understanding (NLU): Determining intent (“I’m thinking about refinancing,” “What’s my status?”) rather than just parsing keywords.

Large language models (LLMs): Generating human-like, context-aware responses that can explain mortgage concepts and handle follow-up questions.

Dialogue management: Tracking what’s been asked and answered so the conversation flows logically and doesn’t repeat.

Orchestration layer: Integrating with your LOS, CRM, pricing engine, appraisal systems, and calendar to read and write data as the conversation unfolds.

Compliance guardrails: Templates, rules, and monitoring that constrain what the agent can say and log every interaction.

Mortgage-native platforms like Marr Labs pre-train these components on mortgage terminology and typical borrower journeys, then fine-tune them to each lender’s products, overlays, and workflows.

What “Agentic” Really Means

Agentic voice AI goes beyond “answering questions.” It:

Decides what to do next: Qualify, schedule, transfer, or follow up later.

Executes tasks: Books appointments, sends disclosures or doc links, updates CRM records, or opens an application in your LOS.

Coordinates participants: Borrower, LO, processor, servicer, real estate agent, and sometimes the title company.

Improves over time: Learns from successful conversations to refine questions, explanations, and routing logic.

This is what turns an AI voice agent from a support tool into a revenue and operations engine. Try a real call for yourself!

Why Mortgage Lenders Need Voice AI Now

Economic Pressures and Margin Squeeze

Origination costs have been stubbornly high, with call centers, manual follow-ups, and QA consuming a disproportionate share of expense per loan. At the same time, lead sources have multiplied, driving up the complexity and cost of converting interest to applications.

Voice AI can materially impact:

Unit economics: Handling a large portion of inbound and outbound volume at a fraction of the cost per minute of human-only teams.

Capacity without headcount: Scaling up during spikes (rate drops, seasonal surges) without hiring and training waves of temporary staff.

Conversion: Responding instantly while competitors still rely on callbacks hours or days later.

Competitive Advantage in a Commoditized Market

When everyone’s rate sheets look similar, speed, certainty, and experience become the differentiators. Lenders using sophisticated voice AI are seeing:

Faster speed-to-lead: AI voice agents like Marr Labs dial in less than a second, qualifying borrowers while they’re still on your landing page or after-hours.

Higher lead utilization: More leads worked, with richer, structured information passed to LOs.

Better borrower experience: Clear expectations, proactive updates, and 24/7 accessibility.

Platforms like Marr Labs lean into this by making their agents indistinguishable from human callers and tightly integrating with mortgage workflows rather than generic contact center scripts. Learn more about why Loan Officers are turning to AI Voice Agents to close more deals.

Integration hub: Connectors to LOS, CRM, pricing, credit, AMS, and ticketing tools.

Compliance and analytics: Monitoring, reporting, audit trails, and custom alerts.

Marr Labs, for example, positions itself as a closed-loop system: calls in, actions executed, and data written back into lender systems, with no open-ended data sharing to external model providers. That’s increasingly important to CISOs and compliance officers.

Core Mortgage Use Cases

AI voice agents deliver the fastest, clearest ROI in a handful of high-volume workflows that blend revenue impact with operational efficiency: working more inbound leads, eliminating scheduling friction, automating document chase, deflecting routine status calls, and scaling servicing outreach with consistent, compliant conversations. Customers love using Marr Labs for use cases such as:

Inbound lead qualification & speed-to-lead: Use Marr Labs’ mortgage-trained agents to answer or call back new leads within seconds, ask a focused set of qualification questions (property, price range, down payment, income, basic credit), write structured data into LOS/CRM, and warm-transfer or schedule with an LO—turning more web and marketplace leads into real conversations without adding headcount.

Appointment scheduling & calendar orchestration: Connect voice agents to LO calendars so they can offer live time slots, book and reschedule calls, and send confirmations and reminders via SMS/email for discovery calls, pre-approvals, conditions reviews, and post-close check-ins—eliminating back-and-forth and keeping pipelines moving.

Document collection & proactive reminders: Have the agent explain conditions in plain language, trigger secure upload links, call or text when new docs are required, confirm what has been received, and log status updates in LOS/CRM, so processors spend less time “doc chasing” and more time moving files to “clear-to-close.”

Application status updates & borrower support: Let borrowers call 24/7 to hear real-time milestones (submitted, in underwriting, conditions outstanding, clear to close, closing scheduled), understand what’s next, and get quick answers to common questions, while complex exceptions are routed to humans with full context.

Servicing outreach & retention: Use agents for high-volume, time-sensitive servicing work—proactive delinquency outreach, explaining high-level options within guardrails, capturing simple intents (“I can make a payment,” “I need help”), answering routine payment/escrow questions, and routing sensitive or complex cases to specialists—backed by full transcripts for QA and regulatory review.

Compliance and Risk Management

Regulatory Landscape Snapshot

AI voice agents must operate within existing law; there is no separate “AI exemption.” Key regimes include:

TRID (TILA-RESPA Integrated Disclosure): Accurate disclosures about costs, APR, and timing.

Fair Lending (ECOA, FHA rules) and disparate impact considerations: No discrimination on protected classes in questions, decisions, or treatment.

FCRA: Proper handling and explanation of credit decisions and adverse action.

GLBA: Data privacy, security, and sharing of borrower personal information.

State-specific rules: Licensing, call recording consent, and disclosure requirements.

How Voice AI Can Improve Compliance

Done correctly, voice AI reduces compliance risk versus relying on human-only processes:

Consistent scripts and disclosures: The AI never “freelances” or forgets mandatory language; changes can be rolled out globally in minutes.

Full call recording and transcripts: Every interaction is searchable and auditable, including system decisions.

Real-time QA: Calls can be scored automatically against compliance rules, with alerts for potential issues.

Encoded fair lending rules: Agents are constrained to use objective criteria and avoid protected characteristics.

Marr Labs and similar vendors highlight their closed data architectures and mortgage-specific compliance models as core differentiators, which resonates with risk and legal teams.

Due Diligence Questions for Vendors

When evaluating platforms:

Can they demonstrate TRID, FCRA, and GLBA-aware conversation flows in production?

How is borrower data stored, encrypted, and isolated?

Can they provide audit logs of decisions and disclosures?

Who bears liability if the agent misstates costs or terms?

How often are compliance rules and templates reviewed and updated?

Implementation and Integration (8–12 Week Plan)

Phase 1: Strategy and Scoping (Weeks 1–2)

Goals:

Define primary use case for phase one (typically inbound lead qualification + scheduling).

Agree on target metrics (e.g., answer rate, speed-to-lead, conversion uplift, and cycle time).

Build an internal steering team across IT, Ops, Compliance, Sales.

Key decisions:

LOS and CRM integration scope for phase one.

Call flows: which phone numbers or queues route to AI vs. humans.

Escalation rules: when to hand off to an LO or call center.

Phase 2: Technical Integration (Weeks 3–4)

Activities:

Connect AI platform to your telephony layer, LOS, CRM, and—optionally—AMS and pricing engine APIs.

Map data fields and event triggers (new lead created, status change, condition added/cleared).

Stand up test environments with synthetic or masked data.

Deliverables:

Working sandbox where internal users can call, see data appear in systems, and verify routing.

Security review and sign-off from IT and InfoSec.

Phase 3: Configuration and Tuning (Weeks 5–6)

Activities:

Configure intents (new purchase, refi, status, payment, etc.) and flows.

Load your loan programs, overlays, and basic pricing rules to enable realistic responses.

Set compliance guardrails based on your policies.

Involving Marr Labs-style teams here gives you a mortgage-specific starting point rather than a blank canvas; most flows are adapted vs. invented from scratch.

User involvement:

Invite 3–5 experienced LOs and processors to test conversations and identify edge cases.

Refine how the agent summarizes calls and passes context when transferring.

Phase 4: Pilot (Weeks 7–8)

Scope:

Route a defined subset of traffic to the AI—e.g., one region, certain marketing campaigns, or after-hours calls.

Monitoring:

Track call volumes, drop-offs, transfer rates, and completion of target actions (qualified, scheduled, updated).

Review a sample of transcripts daily with compliance and sales leadership.

Decision points:

Are borrowers completing flows without confusion?

Are LOs receiving higher-quality, better-documented leads?

Are there any compliance or brand-voice concerns?

Phase 5: Rollout and Optimization (Weeks 9–12+)

Rollout:

Gradually expand coverage to more lines, hours, and use cases as confidence builds.

Train the broader LO and ops teams on how to work with AI-sourced opportunities.

Optimization:

Fine-tune prompts, escalation thresholds, and integration touchpoints based on actual data.

Start layering in additional use cases: status updates, doc chasing, servicing outreach.

Marr Labs and similar vendors often formalize this as a POC-to-production journey so lenders can see measurable impact before going all-in.

Cost per interaction: Handling large call volumes at a lower marginal cost than human-only teams.

Revenue per lead: Higher contact and qualification rates drive better conversion to applications and closings.

Cycle time: Faster movement from inquiry to app, and from conditions to clear-to-close, reduces fallout and improves capacity.

A conservative first-year model often shows 2–4x ROI when combining cost savings with incremental funded loans, especially for lenders with meaningful volume.

KPI Framework

Track a balanced set of metrics:

Operational

AI answer rate (what % of targeted calls does the agent handle?).

Warm transfer rate (what % require human takeover?).

Average handle time per interaction.

Conversion

Lead-to-contact and contact-to-application conversion for AI-handled vs. manual.

Application-to-close rate for AI-qualified vs. non-AI-qualified loans.

Cycle Time

Time from first contact to completed application.

Time from app to doc-complete.

Overall app-to-close timeline.

Compliance and Quality

Percentage of calls auto-flagged for potential compliance issues.

Violation rate in audits before vs. after AI deployment.

Borrower Experience

CSAT or NPS for AI interactions vs. human-only.

Call abandonment rate and after-hours accessibility.

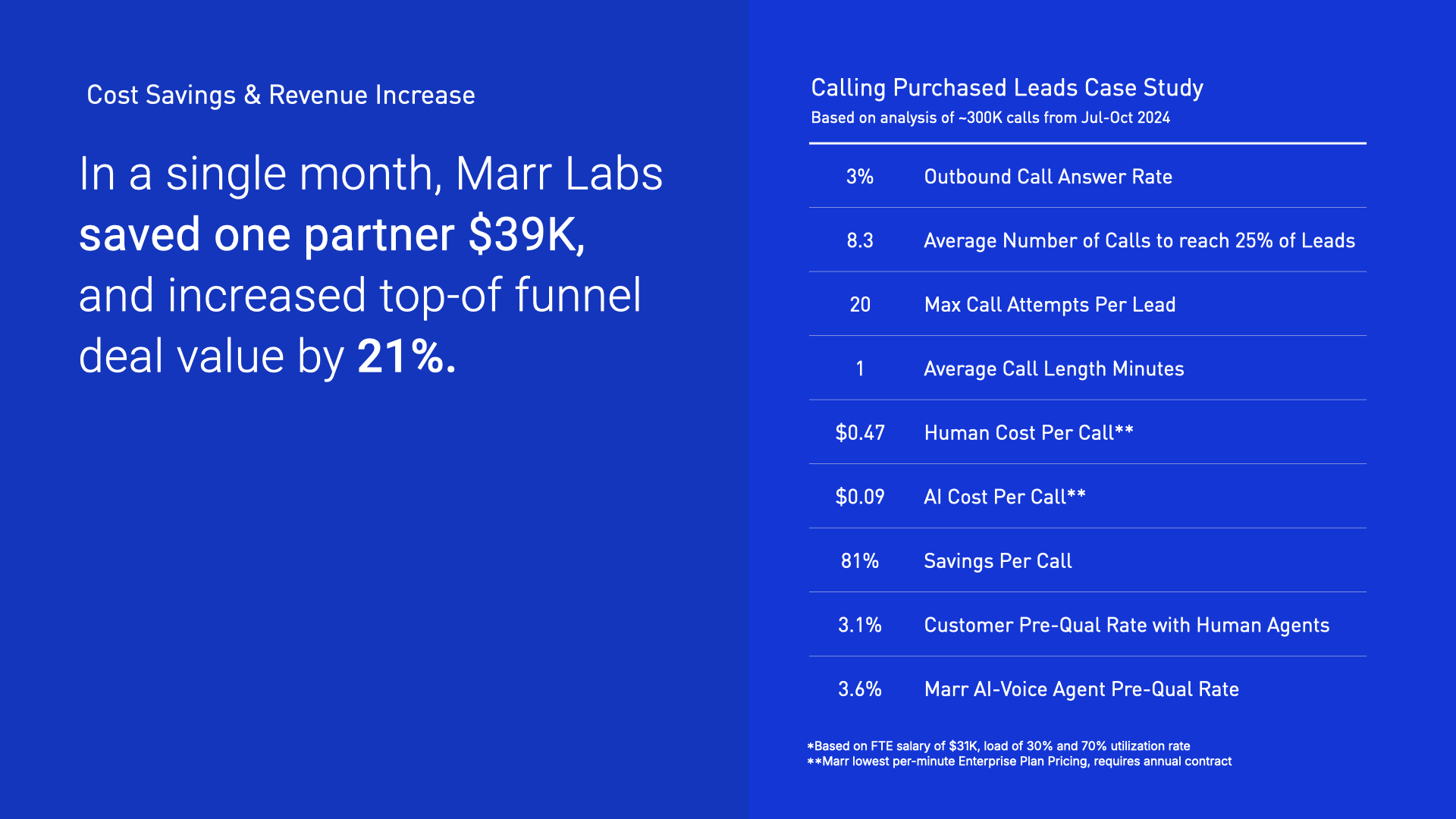

Real-World Impact and Marr Labs Example

Marr Labs and Mortgage-Native Voice AI

Marr Labs focuses specifically on voice AI for mortgage and servicing, rather than generic call center automation. Their solution emphasizes:

Indistinguishable from Human voices and conversational behavior are designed for better borrower interactions.

Deep integration with LOS/CRM workflows and servicing tasks (status calls, payment issues, etc.).

A closed, compliant data architecture that addresses lender concerns around GLBA and model training.

Y Combinator and industry coverage have highlighted Marr Labs as an early mover in building mortgage-specific agentic voice systems that operate as true “digital loan officer assistants.”

Example Outcome: Lead-to-Close Acceleration

In a typical Marr Labs-style deployment with a top lender:

24/7 answer coverage improves contact rates on new leads and inbound calls.

The agent pre-qualifies borrowers, populates key fields, and schedules LO calls.

Document explainer flows and proactive status updates reduce back-and-forth friction.

Across similar deployments, lenders have reported faster application times, higher doc completion, and measurable uplift in volume without proportional headcount increases.

Challenges, Risks, and How to De-Risk Adoption

“Will This Feel Robotic to Borrowers?”

Early generation systems did, and that’s a valid concern. Modern implementations mitigate this through:

High-quality neural voices that mirror human intonation and pacing.

Context-aware conversation that references borrower-specific details.

Easy escape hatches (“I’d like to talk to a person”) and low-friction transfers.

Best practice: test with real borrowers early in the pilot. Many actually prefer fast, clear AI-driven help over long hold times or voicemail loops. Try a call now.

“What If the Agent Misunderstands or Fails?”

No system is perfect. The mitigation strategy is designed with:

Confirmation loops for critical data (“Just to confirm, your approximate credit score is in the 680–720 range?”).

Confidence thresholds: if the model isn’t sure, it transfers.

Continuous monitoring of transcripts to catch edge cases.

Teams that treat voice AI as an evolving system rather than a set-and-forget tool see rapid quality improvements over the first few months.

“What About Regulators and Legal?”

Regulators are paying close attention to AI in lending, but have not banned voice AI usage. They expect:

Clear disclosures when an AI agent is used.

Strong documentation and audit trails.

Demonstrable safeguards against discrimination and misrepresentation.

Bringing compliance and legal into the project from day one, selecting mortgage-native vendors with real audit experience, and starting with lower-risk use cases (e.g., status and scheduling before complex product advice) are practical ways to de-risk.

“Will LOs See This as a Threat?”

Some will, unless you frame and manage it carefully:

Position AI as a “force multiplier” that takes low-value tasks off their plate.

Share data showing higher funded volume per LO in AI-assisted models.

Involve top performers in designing flows so the AI sets them up for success instead of creating friction.

Adoption is strongest where LOs feel they’re getting more, better-qualified at-bats, not being replaced.

The Future of Voice AI in Mortgage

What’s Coming in the Next 3–5 Years

Trends already visible across fintech and mortgage point to:

End-to-end agentic workflows: From first contact to clear-to-close, with AI coordinating most routine steps under human oversight.

Multi-modal support: Borrowers switching fluidly between voice, SMS, and web chat while the same agent context carries through.

Tighter risk integration: Voice agents surfacing risk signals to underwriting and servicing earlier based on conversation patterns.

Clearer regulatory guidance: More explicit standards from CFPB and state regulators on how AI disclosures, fair lending monitoring, and auditability should work.

Is voice AI actually production-ready for large lenders?

Yes. Large banks and top-10 lenders are already running AI voice for customer service and specific lending workflows, including mortgage, with measured gains in speed, containment, and satisfaction when implemented with the right guardrails.

How is this different from chatbots and legacy IVR?

Legacy IVR routes calls via menus and static rules; chatbots handle text with limited context. Voice AI combines real-time speech recognition, LLM-powered conversation, and system integration so it can understand open-ended speech, act on data, and keep context over complex dialogues.

What’s a realistic first-year ROI?

Most lenders with meaningful volume see payback in 3–6 months, combining cost per interaction reductions with increased funded volume from higher contact and conversion rates. Conservative models in 2024–2025 show 2–4x ROI when deployed thoughtfully.

How long does it take to go live?

Typical timelines are 8–12 weeks: 1-2 weeks for scoping, 2–4 for training and testing on your scripts and recordings, 2-3 for a live trial, and 2–3 to start seeing real results. Learn more or start a trial.

Will the AI make lending decisions?

Most lenders use voice AI for qualification and workflow orchestration, not final approval. The agent can suggest products, collect data, and route files; credit decisions typically remain under human or existing automated underwriting systems, which is easier to defend from a compliance standpoint.

How do we handle state-by-state call recording and disclosure laws?

Work with your vendor and legal team to script state-appropriate disclosures and configure telephony to respect one-party vs. two-party consent states. Mature platforms support configurable announcements and logging for this.

What happens if a borrower hates interacting with AI?

Best practice is to provide immediate, easy access to a human: explicit “speak to a person” options, and low-friction transfers when frustration signals are detected. Properly implemented, borrower satisfaction tends to increase because calls are answered quickly and questions are addressed directly.

How does Marr Labs specifically fit into this picture?

Marr Labs focuses exclusively on AI voice agents for mortgage and related financial services, with human-like conversational agents, deep integration into mortgage workflows, and an emphasis on compliance and secure data handling. Lenders use Marr Labs as a mortgage-native way to stand up production-grade voice agents quickly rather than building everything from generic platforms. Read more about the top 10 reasons Lenders trust Marr Labs AI Voice Agents.