AI voice agents are quickly becoming core infrastructure for mortgage lenders that want to work more leads, reduce friction, and stay compliant without growing call-center headcount. The biggest wins are concentrated in a handful of high-leverage workflows where speed, consistency, and integration matter most.

This article breaks down the top 5 AI voice use cases in mortgage lending, with practical examples and how top lenders are using Marr Labs to deploy them in production.

In competitive markets, the first lender to engage often wins the deal. Borrowers submit forms across multiple sites, and if they don’t hear back quickly, they move on. Human teams struggle to follow up instantly on every inquiry, especially after business hours and on weekends.

An AI voice agent fixes this by answering or calling back within seconds, qualifying the borrower, and either transferring live or booking time for the loan officer to call back.

Our mortgage-trained voice agent can:

Instead of loan officers picking up cold or incomplete leads, they start conversations with a clear picture of borrower goals and basic fit.

Coordinating time across borrowers, loan officers, and sometimes real estate agents can be a surprisingly big drag on productivity. Back-and-forth emails, missed calls, and partial voicemails eat into selling time and slow down the pipeline.

Lenders rarely have the staffing to offer true 24/7 scheduling, yet that’s when many borrowers are researching, comparing, and ready to book an initial conversation.

Our AI voice agents connect to your calendar and CRM of choice to:

This works for:

Missing or late documents are one of the most common reasons files stall in underwriting. Processors and loan officers spend countless hours explaining requirements, asking for updated statements, and reminding borrowers what’s still outstanding.

This work is necessary, but it’s also repetitive and highly standardized—making it a perfect fit for AI voice agents.

Our AI voice agents integrated with your LOS can:

This takes pressure off processors and ensures borrowers get consistent, clear communication about what’s needed and why.

One of the biggest call drivers for lenders is simple status questions: “Did you get my documents?” “Has underwriting looked at my file?” “When will I close?” Staff spend a large portion of their day answering these calls or returning voicemails.

The result: borrowers get frustrated when they can’t get quick answers, and teams feel stretched thin by repetitive status updates.

When tied into your LOS and servicing systems, our AI voice agents can:

You can also flip this around: outbound status calls or reminders when key milestones are hit, preventing inbound spikes.

On the servicing side, outreach volume can be high and time-sensitive—especially for delinquency, escrow changes, loss-mitigation options, and retention campaigns. Manual staff can’t always reach every borrower in the right time window, and contact centers face pressure to maintain compliance on every call.

These are high-stakes interactions where both consistency and empathy matter.

Mortgage servicers are using AI voice agents to:

Because every call is transcribed and logged in your CRM, teams can review interactions and regulators can see a complete record of outbound and inbound servicing conversations.

While AI voice agents can support many parts of the mortgage lifecycle, these five use cases consistently deliver outsized returns because they:

Platforms like Marr Labs are built to plug into these use cases quickly, letting lenders start with one or two workflows and expand as value is proven.

If you’re evaluating AI voice agents, a practical approach is:

Ready to address your needs one, or five, use cases at a time? It’s easy to get started! Launch a Marr Labs pilot focused on your highest-impact use case.

%20Are%20Turning%20to%20AI%20Voice%20Agents%20to%20Close%20More%20Deals.jpeg)

Top-producing loan officers are living in a paradox. There have never been more lead sources, referral partners, and channels to manage, but with these tools and technologies come more distractions, callbacks, and repetitive tasks eating into selling time.

Borrowers expect near-instant responses and clear next steps. Over half of borrowers will go with the first lender who contacts them, which means even a great LO can lose deals simply because they were on another call or in a closing. AI voice agents solve this problem by acting as always-on, mortgage-trained assistants that pick up the phone, qualify borrowers, and keep pipelines moving, even when the LO is unavailable.

Marr Labs builds these voice agents specifically for mortgage lenders and originators. They’re designed to sound natural, qualify like an experienced assistant, and hand off to licensed LOs at exactly the right moment, so nothing falls through the cracks.

The highest-intent leads from online forms, rate-quote requests, and marketplace leads go cold quickly if they’re not contacted in minutes.

AI voice agents:

Marr Labs’ POC program is designed to prove this: call leads in under a second after form submit, complete up to 1,000 calls, and show a KPI report on contact rates, qualification, and transfers—without asking loan officers to change CRMs or workflows up front.

For the LO, this means fewer missed opportunities from being in a meeting, at an open house, or simply off the clock.

Most loan officers know the pain of answering the same intake questions multiple times a day and playing calendar tag with borrowers and agents.

AI voice agents can:

Marr Labs integrates directly with CRM and telephony, so the agent’s call results and notes show up exactly where LOs already live, without new logins or extra data entry.

The result: more first conversations start with, “I see you’re looking at a $550k purchase with 10% down and W-2 income. Let’s talk structure,” instead of “So, remind me what you’re trying to do again?”

Every LO knows they “should” follow up more on pre-approvals that went quiet, real estate agent referrals, or old leads that never reached the application stage. In reality, bandwidth and human energy are limited.

AI Voice Agents help by:

Case studies in mortgage and other lending verticals show AI voice agents lifting contact rates and keeping more applications from stalling out simply by being relentless and consistent in follow-up.

For the LO, this is the difference between “I called twice and then moved on” and “every serious borrower heard from your team multiple times, at the right moments, without you living in a dialer.”

Loan officers are at their best when they’re structuring deals, handling objections, and building relationships with borrowers and agents, not when they’re resetting passwords, answering the same rate question for the tenth time today, or manually chasing a bank statement.

Well-designed AI voice agents take on:

Platforms like Marr Labs emphasize “voice agents that work, not just talk”: they’re integrated into borrower workflows, so when the AI says, “We still need your bank statements,” it’s reading that directly from live systems, not guessing.

This reshapes an LO’s day: fewer interruptions and more concentrated blocks of time for the conversations that actually move loans to close.

Borrowers don’t just judge a lender on rate. They judge them on clarity, responsiveness, and whether they feel like someone is “on it.”

AI voice agents:

Marr Labs highlights that the real value isn’t just in a human-sounding voice; it’s in the orchestration of who’s called, what’s said, what’s captured, and what happens next. That’s exactly what borrowers feel: fewer dropped balls, smoother handoffs, and less repetition.

A smoother borrower experience tends to show up where LOs care most: better reviews, more agent referrals, and easier repeat business.

Marr Labs positions its Mortgage Loan Officer Assistant as infrastructure built specifically for lenders and originators, not a generic “voice bot” you have to bend to fit your world.

Key attributes:

For the LO, the benefit is simple: the AI behaves like a smart, compliant assistant that understands mortgage, not a generic bot that needs constant babysitting.

Here’s what it feels like in practice:

These are the moments where deals are won or lost. Marr Labs designs its agents to cover those edges so LOs can focus on being closers and advisors.

Industry experts and AI builders consistently point out that voice AI automates intake, document collection, and follow-ups—not relationship-building, structuring, or negotiation.

In practice:

As one founder quoted in Forbes put it, AI in lending is more like the ATM: it changes the shape of the job but doesn’t eliminate the need for skilled humans.

Borrowers do hate bad automation. They also hate voicemail, unreturned calls, and vague answers. Good voice AI is designed to be:

Marr Labs agents are both useful and human-sounding. LOs and borrowers alike care more about outcome than novelty, so long as the bot gets them where they need to go.

Compliance and LO licensing are crucial considerations. Mature platforms:

Marr Labs positions its system as meeting strict lender and servicer demands: closed-loop data, enterprise security reviews, and pre-trained regulatory alignment, giving compliance officers and LOs confidence that the agent is an asset, not a risk.

If you’re a producing LO, branch manager, or head of sales, the signals that it’s time to explore AI voice agents are straightforward:

Platforms like Marr Labs make it easy to test this with a contained pilot:

If the numbers and LO feedback are strong, you can then expand coverage with confidence.

AI voice agents are quickly becoming standard for high-performing loan officers who want to protect their time and focus on closing more deals without burning out.

Marr Labs’ Mortgage Loan Officer Assistant is built for that exact outcome:

Ready to hear how this would work for your team? Try a call now.

Outbound calling can move fast and, in the mortgage industry, involves important compliance responsibilities, which can add challenges of accuracy at scale. Rocket Mortgage approached Marr Labs with a clear goal; elevate outbound performance in a way that creates a smoother path for customers and supports bankers.

Together, we set out to build an intelligent, efficient outbound tool that works reliably in the real world and adapts with every conversation.

Outbound engagement shapes each customer’s experience through countless small moments, from choosing the right time to reach out, to offering the right message, understanding their needs, easing concerns, and guiding them smoothly to the help they need. Marr Labs’ AI voice agents were built to manage these complexities with consistency, accuracy, and a natural phone experience.

Today, customers move through the process with less friction as agents confirm interest, understand needs, gather essential details and connect them with the right support. The effects carry through operations and banker workflows and ultimately shape a smoother experience for Rocket Mortgage’s clients.

The relationship is driven by tight feedback loops, structured experimentation, and rapid development cycles. Marr Labs and Rocket Mortgage use a disciplined testing framework to evaluate every change — from conversational phrasing to routing logic — ensuring each improvement is validated before it scales.

This ongoing collaboration has produced:

Outbound is less ambiguous and is now becoming a repeatable, measurable, ROI-driving tool.

Marr Labs provides the adaptive agent tool. Rocket Mortgage brings operational depth and a culture of speed and putting the client first. Together, the teams have built a tool that is:

This is more than automation. It is a new model for how AI and humans collaborate to drive value.

Inbound support has evolved rapidly through AI. Outbound is the next major frontier, and Rocket Mortgage is already moving forward. The combination of Rocket Mortgage’s innovation mindset and Marr Labs’ agentic tool is creating a future where:

The future of lending won’t just be faster.

It will be more personal, more intelligent, and more efficient.

And that future is calling.

Most people think of AI on the phone as something simple: the phone rings, the AI agent answers, and the caller explains what they need. And in that world, AI seems pretty capable.

That’s because inbound calls start with clarity.

Someone is calling with a purpose. They already know what they want. Even if they’re frustrated or confused, they’re still driving the conversation in a particular direction.

Outbound calling is the opposite.

And for AI, it’s one of the most complex challenges in voice technology. Many vendors quietly avoid it. The ones who try often end up with calls that sound robotic or stumble the moment a human says something unpredictable.

This is the problem space Marr Labs was built for.

Here’s why outbound calling is so much more complex.

When someone calls their lender, they have an apparent reason. They’re checking a status, asking a question, or trying to get something done. The AI has a starting point.

Outbound conversations begin with uncertainty.

We are interrupting someone’s day. They don’t know who is calling or why. Their first words are often:

“Hello?”

“Who is this?”

“Can this be quick?”

“Is this legit?”

Before Marr Labs can ask a single question, the agent has to establish clarity and trust. Not in a minute. In the first two seconds. If the AI sounds slow, stiff, or unsure, the call is over.

Inbound calls often follow a pattern. Outbound calls do not.

Borrowers answer while walking the dog, sitting in traffic, whispering at work, or juggling their kids. You hear background noise, half-sentences, interruptions, suspicious tones, and sudden changes in energy.

A Marr agent has to process all of this in real time. It must understand what was said, how it was said, and what the borrower is feeling. Then it has to respond naturally, without hesitation.

Generic LLM-based voice tools aren’t built for this. They expect clean audio and long pauses. Outbound gives them the opposite.

In mortgage lead conversion, seconds matter.

When a borrower submits a LendingTree form or a similar service, Marr Labs can call them within one second.

That tiny window requires a surprising amount of coordination: receiving the lead, placing the call, connecting, detecting that the person has said “hello,” and then speaking with lifelike timing.

All of this has to happen at human speed. If the AI hesitates, the borrower loses trust.

Humans are naturally good at this. AI systems are not unless they’re designed for it from the ground up.

Inbound callers give some grace because they chose to call.

Outbound call recipients do not.

They evaluate you immediately. Do you sound friendly? Competent? Confident? Are you wasting their time?

An outbound AI agent must match tone, pace, and energy instantly. It needs to sense irritation, confusion, interest, or distraction and adjust in real time. It needs to know when to move forward and when to slow down.

This is why our agents are trained with real scripts, honest borrower conversations, and real mortgage workflows.

Outbound calls require emotional intelligence.

Outbound dialing involves a much more complex regulatory environment than inbound.

There are calling windows, do-not-call lists, licensing limits, disclosures, recording rules, and escalation paths. The agent must follow all of these perfectly, without exception.

One mistake is all it takes to create exposure.

Most general-purpose AI systems aren’t built with this level of structure or consistency. Marr Labs is.

A bad inbound call is a customer experience problem.

A bad outbound call is a revenue problem.

Every missed connection or awkward moment can mean:

This is why reliability matters so much. Marr Labs delivers enterprise-grade uptime and high task completion rates in environments where the stakes are real.

Most voice AI platforms are built around a simple idea: the AI listens, thinks, and talks.

But outbound calling requires far more than that.

A Marr agent coordinates:

All at the same time, and fast enough to feel natural.

This is what makes outbound calling so hard for AI and why Marr Labs invests so deeply in solving it.

Outbound calling is messy and high-stakes, but it is also where lenders gain enormous leverage. It’s the part of the business that actually scales revenue, not just service. And that’s why it became our specialty.

Mortgage lending is hitting a structural reset. Borrowers expect instant, 24/7 answers, Loan Officers are juggling more communications channels than ever, and the cost to originate a loan keeps creeping up. AI voice agents are emerging as one of the few levers that can move all three constraints–speed, cost, and borrower experience—at once.

For top mortgage lenders, voice AI is no longer a novelty. It’s becoming infrastructure: qualifying leads in minutes, orchestrating complex workflows, and enforcing compliance at scale. Early adopters are already reporting double-digit improvements in worked opportunities and cycle time compression measured in days.

This guide is written for modern mortgage executives, technologists, and revenue leaders who want a complete picture: what AI voice agents are, how they work with your LOS and CRM, how to stay compliant, what implementation really looks like, where the risks are, and how to measure ROI.

Legacy IVRs and basic phone trees were built to route calls and reduce headcount, not to understand borrowers. They forced people into rigid menus and handed off context-poor calls to overloaded loan officers.

Modern AI voice agents are different in three fundamental ways:

In other words, they behave less like automated receptionists and more like digital loan officer assistants that operate 24/7.

Under the hood, a production-ready voice agent combines:

Mortgage-native platforms like Marr Labs pre-train these components on mortgage terminology and typical borrower journeys, then fine-tune them to each lender’s products, overlays, and workflows.

Agentic voice AI goes beyond “answering questions.” It:

This is what turns an AI voice agent from a support tool into a revenue and operations engine. Try a real call for yourself!

Origination costs have been stubbornly high, with call centers, manual follow-ups, and QA consuming a disproportionate share of expense per loan. At the same time, lead sources have multiplied, driving up the complexity and cost of converting interest to applications.

Voice AI can materially impact:

When everyone’s rate sheets look similar, speed, certainty, and experience become the differentiators. Lenders using sophisticated voice AI are seeing:

Platforms like Marr Labs lean into this by making their agents indistinguishable from human callers and tightly integrating with mortgage workflows rather than generic contact center scripts. Learn more about why Loan Officers are turning to AI Voice Agents to close more deals.

At a high level, here’s what happens when a borrower calls a lender running a modern voice AI stack:

Marr Labs, for example, positions itself as a closed-loop system: calls in, actions executed, and data written back into lender systems, with no open-ended data sharing to external model providers. That’s increasingly important to CISOs and compliance officers.

AI voice agents deliver the fastest, clearest ROI in a handful of high-volume workflows that blend revenue impact with operational efficiency: working more inbound leads, eliminating scheduling friction, automating document chase, deflecting routine status calls, and scaling servicing outreach with consistent, compliant conversations. Customers love using Marr Labs for use cases such as:

AI voice agents must operate within existing law; there is no separate “AI exemption.” Key regimes include:

Done correctly, voice AI reduces compliance risk versus relying on human-only processes:

Marr Labs and similar vendors highlight their closed data architectures and mortgage-specific compliance models as core differentiators, which resonates with risk and legal teams.

When evaluating platforms:

Goals:

Key decisions:

Activities:

Deliverables:

Activities:

Involving Marr Labs-style teams here gives you a mortgage-specific starting point rather than a blank canvas; most flows are adapted vs. invented from scratch.

User involvement:

Scope:

Monitoring:

Decision points:

Rollout:

Optimization:

Marr Labs and similar vendors often formalize this as a POC-to-production journey so lenders can see measurable impact before going all-in.

You can get started with a POC today!

Voice AI affects three levers simultaneously:

A conservative first-year model often shows 2–4x ROI when combining cost savings with incremental funded loans, especially for lenders with meaningful volume.

Track a balanced set of metrics:

Marr Labs focuses specifically on voice AI for mortgage and servicing, rather than generic call center automation. Their solution emphasizes:

Y Combinator and industry coverage have highlighted Marr Labs as an early mover in building mortgage-specific agentic voice systems that operate as true “digital loan officer assistants.”

In a typical Marr Labs-style deployment with a top lender:

Across similar deployments, lenders have reported faster application times, higher doc completion, and measurable uplift in volume without proportional headcount increases.

Early generation systems did, and that’s a valid concern. Modern implementations mitigate this through:

Best practice: test with real borrowers early in the pilot. Many actually prefer fast, clear AI-driven help over long hold times or voicemail loops. Try a call now.

No system is perfect. The mitigation strategy is designed with:

Teams that treat voice AI as an evolving system rather than a set-and-forget tool see rapid quality improvements over the first few months.

Regulators are paying close attention to AI in lending, but have not banned voice AI usage. They expect:

Bringing compliance and legal into the project from day one, selecting mortgage-native vendors with real audit experience, and starting with lower-risk use cases (e.g., status and scheduling before complex product advice) are practical ways to de-risk.

Some will, unless you frame and manage it carefully:

Adoption is strongest where LOs feel they’re getting more, better-qualified at-bats, not being replaced.

Trends already visible across fintech and mortgage point to:

Lenders who build voice AI capabilities now will be better positioned to adopt these next layers without starting from scratch.

Yes. Large banks and top-10 lenders are already running AI voice for customer service and specific lending workflows, including mortgage, with measured gains in speed, containment, and satisfaction when implemented with the right guardrails.

Legacy IVR routes calls via menus and static rules; chatbots handle text with limited context. Voice AI combines real-time speech recognition, LLM-powered conversation, and system integration so it can understand open-ended speech, act on data, and keep context over complex dialogues.

Most lenders with meaningful volume see payback in 3–6 months, combining cost per interaction reductions with increased funded volume from higher contact and conversion rates. Conservative models in 2024–2025 show 2–4x ROI when deployed thoughtfully.

Typical timelines are 8–12 weeks: 1-2 weeks for scoping, 2–4 for training and testing on your scripts and recordings, 2-3 for a live trial, and 2–3 to start seeing real results. Learn more or start a trial.

Most lenders use voice AI for qualification and workflow orchestration, not final approval. The agent can suggest products, collect data, and route files; credit decisions typically remain under human or existing automated underwriting systems, which is easier to defend from a compliance standpoint.

Work with your vendor and legal team to script state-appropriate disclosures and configure telephony to respect one-party vs. two-party consent states. Mature platforms support configurable announcements and logging for this.

Best practice is to provide immediate, easy access to a human: explicit “speak to a person” options, and low-friction transfers when frustration signals are detected. Properly implemented, borrower satisfaction tends to increase because calls are answered quickly and questions are addressed directly.

Marr Labs focuses exclusively on AI voice agents for mortgage and related financial services, with human-like conversational agents, deep integration into mortgage workflows, and an emphasis on compliance and secure data handling. Lenders use Marr Labs as a mortgage-native way to stand up production-grade voice agents quickly rather than building everything from generic platforms. Read more about the top 10 reasons Lenders trust Marr Labs AI Voice Agents.

Marr Labs is proud to announce its collaboration with Figure, a pioneering force in mortgage technology. This partnership marks a significant step forward in leveraging AI voice agents to enhance borrower communications, streamline processes, and improve overall client experience.

By integrating cutting-edge voice AI technology into Figure’s mortgage operations, we are setting a new standard for what’s possible in the lending industry—making interactions more natural, efficient, and impactful for borrowers and lenders alike.

Marr Labs builds better-than-human AI voice agents that respond intelligently, and are purpose-built for the strict demands of mortgage lending: from lead response and qualification to warm transfers to loan officers and ongoing borrower support.

Our agents plug into lenders’ existing tech stack (CRM, LOS) to capture data, trigger workflows, and keep borrowers engaged, all while operating in a secure, closed-loop environment with compliance baked in. This means lenders can scale outreach while reducing costs, all without sacrificing the quality or consistency of borrower conversations.

Getting started with Marr Labs is intentionally simple: there is no need for technical expertise or complex implementation projects. In just a few minutes, you can:

Questions? Reach out to our Mortgage AI Specialists.

The Information recently spotlighted a wave of startups building AI-powered voice agents across industries, from restaurants to fintech to mortgage lending. It’s exciting coverage for a technology that’s quietly matured over the past 12 to 18 months. But amid all the excitement, something more fundamental is happening: the real innovation isn’t just in the voice. It’s in the workflow.

Advances from OpenAI, Deepgram, Google, and others have made real-time, human-like voice interaction finally possible and affordable. What separates a flashy demo from a real business solution isn’t better speech quality. It’s better process design.

At Marr Labs, we’ve seen this firsthand. We build voice agents for mortgage lenders that don’t just “talk.” They work. Our agents qualify borrowers, capture key data, and route the call while staying compliant and integrated with client CRMs and telephony systems. The value isn’t in the voice alone. It’s in the orchestration: who gets called, when, under what conditions, what’s said, what’s captured, and what happens next.

In other words, the agent is just the interface. The magic is in what it connects to and how it fits into the business process.

That’s where many new entrants get it wrong. It’s tempting to focus on the model, the voice, the latency numbers. And yes, those matter. But when voice AI gets deployed in the real world — in mortgage, healthcare, logistics, or hospitality — it meets a wall of operational complexity:

Solving for those is where the true differentiation lies.

We’ve learned, for example, that a one-second delay in warm-transferring a borrower can mean a lost lead. That the wrong phrasing during a qualification call can trigger regulatory issues. That transferring too early or too late undermines trust. Designing for these details and iterating them over time is what makes a voice agent effective.

The market is starting to see that. The Information noted that companies like Marr Labs are already running real-time qualification calls on behalf of lenders, not as a proof of concept, but as a core operational tool. And that’s just the beginning. The winners in this space won’t be the ones with the smoothest-sounding bots. They’ll be the ones that make voice AI invisible, woven into the flow of business, supporting people and processes without getting in the way.

Voice AI isn’t a product. It’s infrastructure. And the best infrastructure disappears.

Last week, Marr Labs CEO Dave Grannan joined Josh Reicher, Chief Digital Officer at Cenlar FSB , and moderator Ruth Lee for a deep dive into how AI voice technology is used today across the mortgage industry. This wasn’t another high-level discussion about chatbots or IVR. It was a practical look at how human-like voice agents solve real problems—from lead conversion to borrower support.

Here are some takeaways from the conversation: use cases, lessons learned, and where AI voice is headed.

Dave Grannan opened with a stat that caught everyone’s attention: over half of borrowers go with the first lender who contacts them. That means speed is everything if you're buying leads from sources like LendingTree or NerdWallet.

AI voice agents can engage a lead within one second of submission, qualifying them, gathering details, and transferring to a licensed loan officer. The big unlock? You don’t need more staff to do it.

“You can turn on 1,000 AI agents right now and turn them off in an hour. That kind of flexibility is impossible with human teams.”

— Dave Grannan, Marr Labs CEO

The webinar featured a demo of a Marr Labs AI Voice Agent qualifying a borrower for a home equity loan and then making small talk to keep the caller engaged until a live loan officer joined the call. Grannan noted that this warm handoff significantly reduces call abandonment.

AI voice agents are designed to sound natural, respond intelligently, and never get tired or frustrated, giving borrowers a more consistent experience than traditional call centers.

Josh Reicher shared how Cenlar is using AI to improve operational service efficiency.

One use case: answering common borrower questions (like requests for a 1098 form) without human involvement. The key is matching the right level of complexity to the right tool.

“Most digitally savvy homeowners prefer to self-serve. If they can get an answer in one call, 24/7, they’re happy.”

— Josh Reicher, Cenlar

Both Dave Grannan and Josh Reicher emphasized that AI voice should empower, not replace, human agents—especially in emotionally charged or complex situations. Today’s AI voice agents can recognize the right moment to get out of the way.

Here’s how that works:

“If someone gets annoyed or asks to speak to a human, we don’t fight it—we route the call. It’s about getting the task done, not pretending the AI can do everything.”

— Dave Grannan, Marr Labs CEO

This hybrid approach ensures borrowers feel supported, while human reps focus where they’re most needed.

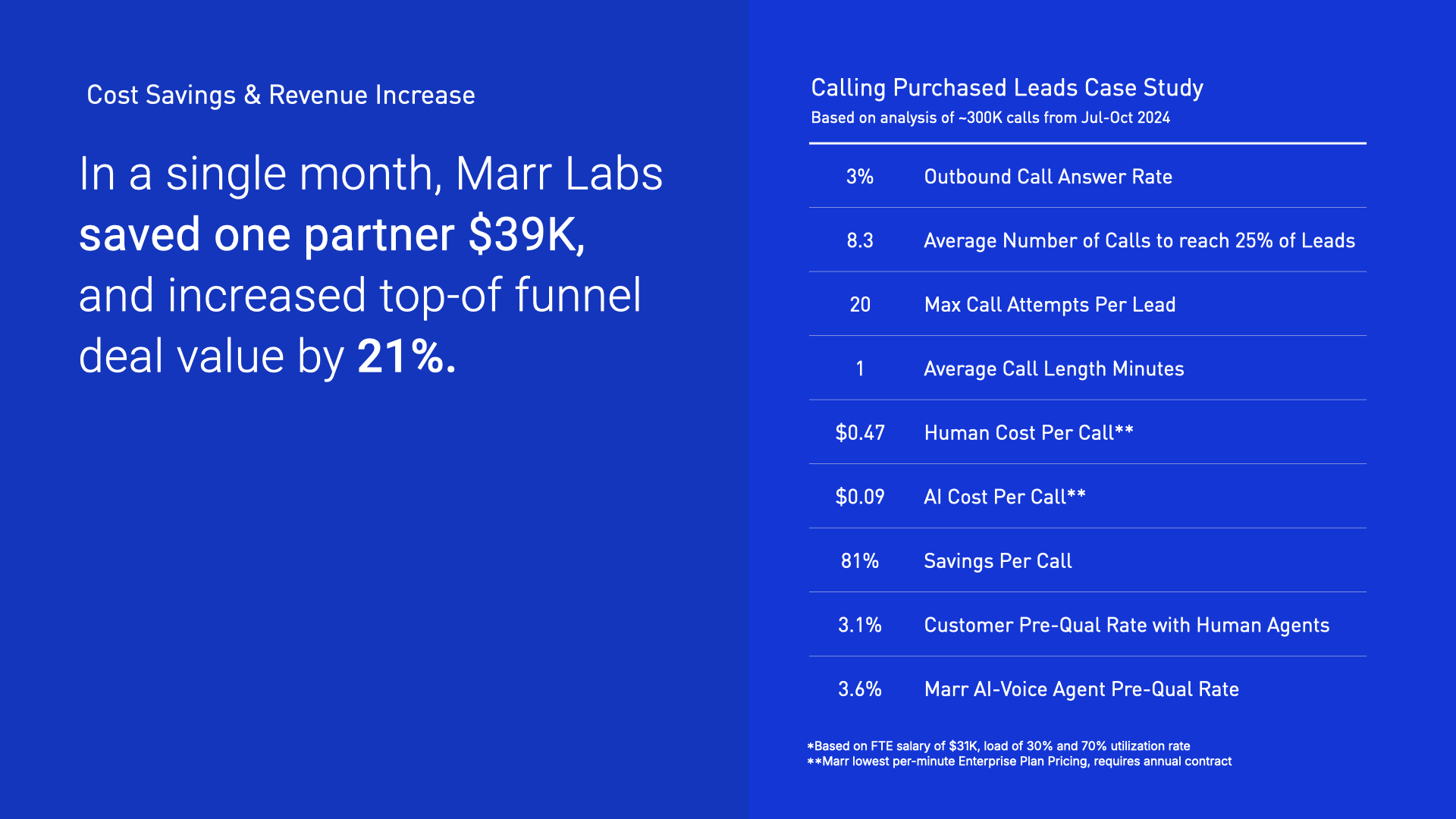

Grannan shared results from a recent case study across 300,000 calls:

Reicher echoed the value of starting small and measuring impact. “If the tool helps your team spend more time with borrowers and less time on busywork, it pays off fast,” he said.

Looking ahead, both speakers pointed to agentic AI as the next evolution—tools that can handle entire workflows with minimal supervision.

“Voice AI is no longer about routing or menus. It’s about completing real tasks—accurately, efficiently, and with empathy. ”

— Dave Grannan, Marr Labs CEO

Watch the full webinar recording for live demos, practical advice, and an inside look at what leading mortgage teams are doing with AI voice.

chris at marrlabs.com

Over the past year, the team at Marr Labs has had conversations with dozens of mortgage lenders. We’ve heard a remarkably consistent message: lenders need a faster, more effective, and compliant way to engage with borrowers and prospects. Speed matters. So does persistence. And staying on message—every time—can make the difference between a closed loan and a missed opportunity. But let’s be honest: even the best human teams have limits.

That’s where the Marr Labs AI Call Center steps in. Our virtual voice agents specialize in bridging the gap, ensuring that borrowers are connected with the right human loan officers— faster and more effectively than ever before.

Think of it as a perfect partnership: the efficiency and consistency of AI, paired with the expertise and personal touch of human loan officers. When lenders experience the “better than human” precision and performance of our AI voice agents—and see how it drives faster borrower engagement and more closed loans—they get it. It’s not just a solid business case. It’s a game-changer.

That’s why we’re proud to have Better Mortgage as our launch partner and flagship customer. We’re grateful for their partnership and their spirit of innovation. Curious to see what’s possible? Try the Marr Labs AI Call Center for yourself at marrlabs.com/mortgage-loa or book an intro call with me anytime here.